Debt can feel overwhelming, especially when it comes with high interest rates that make it harder to get ahead. In this guide, we’ll break down practical, realistic strategies to help you pay off your consumer debt faster and smarter without needing a big income boost or unrealistic sacrifices.

If you’ve ever felt like you’re throwing money into a bottomless pit just to cover interest, or like you’re stuck making payments with no end in sight you’re not alone. Debt can be a heavy burden, weighing on your financial freedom and your peace of mind.

Debt has become so “normal” that many people think of it as just another bill. But actually, the longer it lingers, the more interest you’re paying, and that’s money that could be working for you instead of your lender.

1. Why Paying Off Debt Faster is Important

Save on Interest

Interest is where debt gets expensive, and the higher the interest rate, the more money you lose over time.

Frugal Tip: Focus on high-interest debts first like credit cards, payday /personal loans, or high interest car loans. Paying those off quickly saves you the most money because those interest rates compound fast.

Example:

- Credit card balance: $5,000

- Interest rate: 20% APR

- If you only make minimum payments (~$125/month), you’ll take more than 5 years to pay it off and spend over $10,000 in total.

That’s double your original debt just because of interest!

Reduce Financial Stress

Debt isn’t just about numbers it’s about the stress of living paycheck to paycheck or worrying whether you can cover an emergency. Paying it off faster gives you emotional relief and confidence.

Free Up Cash Flow

When debt payments disappear, you gain breathing room in your budget. Imagine an extra $400 each month going toward savings, a family trip, or investments that grow instead of drain.

2. Key Strategies to Pay Off Debt Faster

Not every strategy works for everyone, but these proven methods can speed up your progress:

Avalanche Method

- How it works: Pay off debts with the highest interest rates first (while making minimums on the rest).

- Best for: Saving the most money on interest.

- Example: Attack the 24% APR credit card before the 6% auto loan.

Why this matters: Since high-interest loans cost you the most, eliminating them first keeps more money in your pocket.

Snowball Method

- How it works: Pay off the smallest balance first to build momentum.

- Best for: Staying motivated with quick wins.

- Example: Knock out that $600 store card before tackling the $3,000 personal loan.

Balance Transfer or Refinancing

- Transfer credit card debt to a 0% APR promo card (if you qualify).

- Refinance a personal loan or auto loan to a lower rate.

Frugal Tip: Only transfer balances if you can pay them off before the promo ends. Otherwise, the interest can jump back up higher than before.

Side Income

Sometimes trimming expenses to free up money to pay down debt faster isn’t enough. Boost your repayment power by:

- Freelancing or gig work (rideshare, tutoring, freelancing online)

- Selling unused items

- Offering services like babysitting or lawn care

Check out our blog post 15 Side Hustles You Can Start with Little to No Skill

3. How to Calculate Payments to Fit Your Budget

Debt-to-Income Ratio

Your DTI ratio shows how much of your income goes toward debt:

- Formula: (Monthly Debt ÷ Monthly Income) × 100

- Example: $1,200 debt ÷ $4,000 income = 30% DTI

Lowering your DTI gives you flexibility and reduces financial stress.

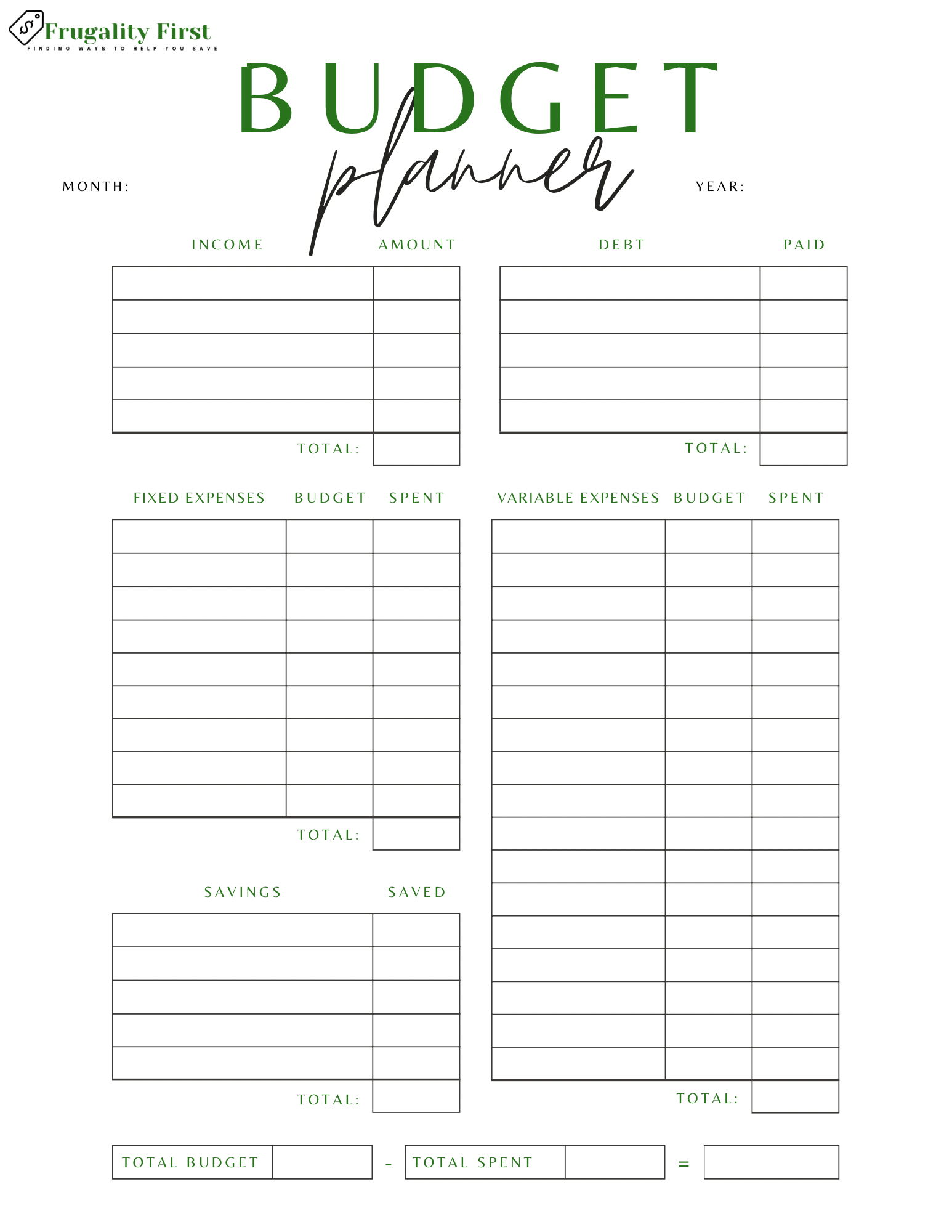

Setting a Budget

- List your income.

- Subtract fixed bills.

- Identify what you can cut (subscriptions, dining out, impulse spending).

- Redirect that money toward debt.

Frugal Tip: Even $50 extra a month speeds up your payoff. That’s one less dinner out or three fewer coffee runs a week.

Using Online Calculators

Tools like NerdWallet’s Debt Snowball Calculator or undebt.it let you compare avalanche vs. snowball and see how much faster you’ll be debt-free by paying just a little more each month.

4. How to Calculate Interest Savings

Why Interest Savings Matter Most with High-Interest Debt

High-interest debt (like credit cards at 20–30% APR) grows faster than low-interest debt (like a 4% car loan). Paying those off early prevents years of wasted money.

Formula for Simple Interest:

Total Interest = Principal × Rate × Time

In reality, credit cards use compounding interest, which makes it even more expensive, but this formula gives you a ballpark.

Example Scenario

- Loan: $10,000 at 10% APR, 5 years

- Minimum Payment: $212/month

- Total Interest: ~$2,700

If you add $50 extra each month, you save over $800 in interest and pay it off a year earlier.

Frugal Tip: Even small extra payments on high-interest debts first save the most money long-term.

5. Tools to Help You Stay on Track

- Debt Repayment Apps: Debt Payoff Planner, Tally, or Undebt.it

- Spreadsheets: DIY with Excel/Google Sheets to track balances and celebrate milestones

- Set Milestones: Pay off 25% of your debt? Celebrate. Knock out one credit card? Celebrate.

Frugal Tip: Download our Free Budget Planner Worksheet

{kind=link}

6. How to Make Paying Off Debt Part of Your Lifestyle

Adopt a Mindset of Financial Freedom

Debt payoff is an investment in your future. Each payment is a step closer to peace of mind and flexibility.

Cut Unnecessary Expenses

- Cancel subscriptions you don’t use.

- Limit dining out.

- Use cash-back or rebate apps to stretch your money.

Celebrate Small Wins

Don’t wait until you’re 100% debt-free. Celebrate progress along the way to stay motivated.

Key Takeaway

Paying off debt faster and smarter isn’t just about the numbers. It’s about freedom, stress relief, and taking back control of your financial future.

- Focus on high-interest debt first, that’s where you save the most money.

- Use strategies like avalanche, snowball, or side hustles to increase income.

- Calculate realistic payments and stick with a budget.

- Track progress with apps or spreadsheets and celebrate milestones.

The best time to start is today. Whether it’s an extra $20 payment, setting a budget, or downloading a debt tracker, every step forward matters.

Bonus: Common Mistakes to Avoid

- Missing Minimum Payments → late fees + credit score damage

- Focusing Only on Debt → don’t forget emergency savings or retirement

- Overcommitting Your Budget → realistic progress beats burnout

With focus, consistency, and a frugal mindset, you can pay off debt faster, save thousands in interest, and build the future you’ve been dreaming of.

Need more budgeting tools? Shop our Budget Planner: A Guided Workbook to Take Control of Your Money

Disclaimer: The financial tips and strategies provided in this document are for informational

purposes only and should not be considered financial advice. While every effort has been made to

ensure the accuracy of the information, individual financial situations vary. It is recommended that

you consult with a qualified financial advisor before making any financial decisions. The author and

publisher are not responsible for any losses or damages that may arise from the use of this

information.